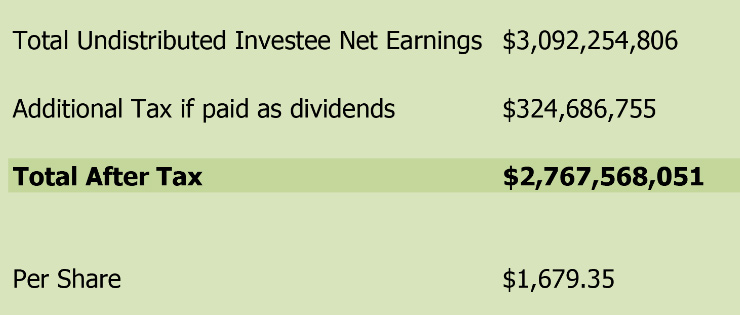

Berkshire Hathaway Performance

Portfolio manager’s Letter July 2010

Berkshire Hathaway performance has out-performed the S&P 500

Berkshire Hathaway performance this year has out-performed the S&P 500 this year by about 27%, so Losch Management Company’s portfolios, which had been heavily dependant on Berkshire Hathaway performance, have been doing well compared to the overall stock market. Most of Berkshire Hathaway performance was the result of the 50 for one split of its “B” shares and its inclusion in the S&P 500 Average. Last month’s announcement that Berkshire Hathaway would also be included in the Russell 3000 and 1000 averages has been responsible for the stock’s recent rally.

Because the recent rally is not based only on earnings improvement, and that the hurricane season has not generally been a strong period for the stock, this rally will likely be temporary. We reduced our overweight position in Berkshire Hathaway for two reasons. First, the recent correction in the overall stock market has left us with a lot of good quality stocks that are currently selling at attractive prices. Second, the prospect of a bad hurricane season and a lot of petroleum sloshing around in the Gulf of Mexico may provide us with an interesting indicator for Berkshire Hathaway performance.

Goldman Sachs

Is Goldman Sachs a fat pitch? At six times the last twelve months’ earnings and 1.6 times book, it certainly appears cheap. The question is this: do 2009’s earnings have anything to tell us about the company’s future, and its impact on Berkshire Hathaway performance?

Michael Lewis, in his book “The Big Short”, says Wall Street is over. While this may be an overstatement, I agree that Wall Street will never be the same (hopefully). Will Goldman Sachs return to the glory of its recent past, or has its business model been blown, and what will be the impact on Berkshire Hathaway Performance?

If commercial banks are forced to give up their trading book, their derivative trading, and their private equity business, this will hurt Goldman Sachs. However, the company’s main business has traditionally been in underwriting and in mergers and acquisitions. These are areas where Goldman Sachs may well be better off in the future because their own greed has eaten a lot of their competition.

Investors are worried about the impact of regulation, but I think the bigger question for Goldman Sachs is what lessons will be taken from the company’s near death experience. The old proverb that should apply is “that which does not kill us will make us stronger”. There is, of course, no guarantee that Goldman Sachs will learn from this market turbulence, but no one has ever accused them of being stupid.

If Goldman Sachs can learn from their mistakes and bad behavior, concentrate on their core franchise of underwriting merger business, they will still have a name that is the best in the industry. They will have a positive effect on Berkshire Hathaway Performance. If they do this, they can be a better company in the future without the derivative business, with its conflicts of interest and excess leverage.

There was a lot of stuff going on at Goldman Sachs and at their Wall Street cronies that our economy really does not need. It is a fairly easy guess that Congress will do some things that are likely to damage Goldman Sachs’s bottom line in the short term, and it will be interesting to see how Goldman Sachs reacts.

Lewis thinks that Goldman Sachs should be broken up and that its’ high-risk businesses sold to hedge funds. He believes that compensation plans for traders need to reflect the risks the traders are taking. This leads him to the conclusion that high-risk trades belong in a partnership because then the people taking the risk have all of their skin in the game. I do not know if this is realistic, but I have to admit it sounds like a good idea, and might influence Berkshire Hathaway Performance.

It would be similar to Buffett’s idea that CEO’s of busted banks should end up broke. But, Lewis has a more elegant solution because, with his way, all of the big players, not just the CEOs, would end up broke; this has to be a better result than today where just the shareholders ending up broke.